Technology acceptance models such as TAM and UTAUT are widely used to explain why people adopt new technologies. They are robust, elegant, and easy to apply. But are they still reliable when technologies become more complex and interaction modes change?

In our new open-access paper, we systematically test the robustness of classic acceptance models across different interaction perspectives and comparable technologies. The core insight is simple but consequential: acceptance is not only about usefulness and ease of use – it is also about how people perceive their role in using a technology.

Active vs. passive interaction matters

We show that acceptance relationships change depending on whether users experience a technology as something they actively control or passively observe. Under these conditions, classic models lose stability. Constructs that are usually considered robust behave differently across perspectives.

Introducing Usage Perception

To address this, we extend existing models with the construct Usage Perception (UP). UP captures how users cognitively frame their interaction with a technology. The result:

more stable path relationships

higher theoretical coherence

improved explanatory power across technologies

Why this is relevant

For AI systems, autonomous technologies, XR, and emerging mobility concepts, acceptance cannot be fully explained without accounting for perception of use. This has implications for:

Automated driving is becoming increasingly relevant in research, industry, and society. Alongside technological development, questions concerning ethical decision-making and user acceptance are gaining importance. The bachelor thesis by Lea Merz examines which ethical factors influence the user acceptance of automated driving systems and how these factors can be connected to an established technology acceptance model.

Background: Acceptance Models and the Research Gap

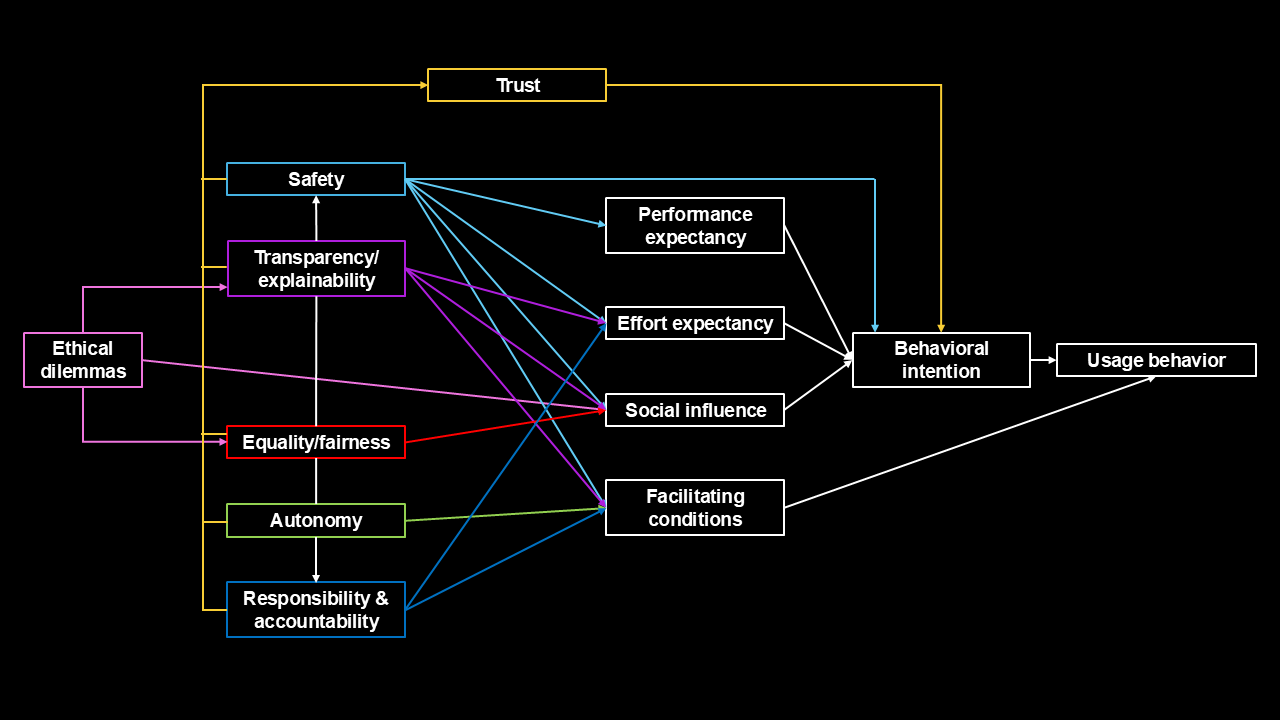

The Unified Theory of Acceptance and Use of Technology (UTAUT) by Venkatesh et al. (2003) is a widely used model for explaining technology adoption, focusing on performance expectancy, effort expectancy, social influence, and facilitating conditions.

However, research on automated driving has shown that these components alone are not sufficient, as automated vehicles operate in safety-critical situations and must make ethically sensitive decisions. Ethical dimensions such as transparency, responsibility, fairness, and user autonomy have therefore become increasingly relevant. Despite that they remain largely overlooked in existing acceptance research, which tends to emphasize functional and technical system characteristics.

To address this gap, the bachelor thesis integrates ethical aspects into the UTAUT framework and examines their relevance for user acceptance in the context of automated driving.

Methodology

To investigate which ethical factors shape acceptance, the thesis uses a qualitative research design based on nine expert interviews. The experts come from fields such as automated driving, ethics, mobility research, and technology acceptance.

The material was analyzed using structured qualitative content analysis, leading to a systematic categorization of ethically relevant elements that influence acceptance.

Key Ethical Factors Identified in the Study

The results of the content analysis highlight several key categories:

Safety

Safety emerged as a central theme, including physical safety, subjective perceptions of safety, system reliability, the protection of human life, and the system’s ability to adapt traffic-appropriate and socially confirming. These elements reflect both technical safety requirements and users’ personal feelings of security during automated driving.

Autonomy

Autonomy refers to the user’s ability to maintain control, intervene when necessary, and voluntarily decide when to use automated driving functions. The category also captures the importance of allowing users to choose the degree of automation according to their individual preferences and comfort levels.

Responsibility and Liability

The category of responsibility and liability addresses questions about accountability in the case of system malfunctions and responsibility for accidents involving automated vehicles. It includes issues such as the distribution of responsibility between users, manufacturers, and system developers, and the clarity of responsibility assignments in safety-critical scenarios.

Transparency and Explainability

Transparency and explainability concern the availability of understandable information about system behavior, insight into system functions and limitations, and clarity regarding the decision-making processes of automated vehicles. These aspects relate to users’ need to comprehend how the system operates and what its functional boundaries are.

Ethical Dilemmas and Decision Conflicts

This category describes system decisions in morally challenging situations, including situations in which collisions are unavoidable. It includes considerations about how automated vehicles should handle conflicting values and prioritize different outcomes in ethically sensitive traffic scenarios.

Fairness and Equal Treatment

Fairness and equal treatment refer to the ethical requirement that automated vehicles avoid discriminatory behavior, consider different groups of road users equally, and prevent biases within system decision-making. These aspects highlight the importance of ensuring that automated systems act in a manner that is impartial and inclusive across diverse traffic situations.

Trust

Trust emerges as a cross-cutting category influenced by perceived safety, transparency, and the degree of user control. It encompasses several elements, including confidence based on system experience, safe and predictable drivingbehavior, transparent communication between the vehicle and the user, and clarity regarding responsibility assignments.

Extension of the UTAUT Model

Based on the identified categories, the thesis develops an extended UTAUT model that incorporates ethically relevant factors into the existing acceptance framework. The model builds on the original UTAUT components and adds categories such as safety, autonomy, transparency, responsibility, fairness, and trust to more comprehensively reflect the specific characteristics of automated driving systems. This extension follows the theoretical structure of UTAUT and positions the ethical dimensions in relation to the empirical findings of the study.

Figure 1. Author’s own illustration based on Venkatesh et al., 2003, p. 447).

Conclusion

The bachelor thesis by Lea Merz offers a structured presentation of ethical factors that influence the acceptance of automated driving systems. By integrating theoretical concepts from the UTAUT framework and ethical research with qualitative expert insights, the study provides a clearer understanding of relevant user expectations in the context of automated mobility.

Future research should further examine the extended model, for example through quantitative approaches or structural equation modeling, in order to empirically validate the relationships between the identified ethical factors, trust, and user acceptance.

Reference

Venkatesh, N., Morris, M. G., Davis, N., & Davis, N. (2003). User Acceptance of Information Technology: Toward a Unified View. MIS Quarterly, 27(3), 425 478. https://doi.org/10.2307/30036540

Artificial intelligence is no longer a futuristic vision but a tangible part of financial reality. Financial institutions increasingly rely on AI technologies for tasks ranging from credit scoring to fraud detection. Yet, the crucial question remains: How willing are people to delegate financial decision-making to machines?

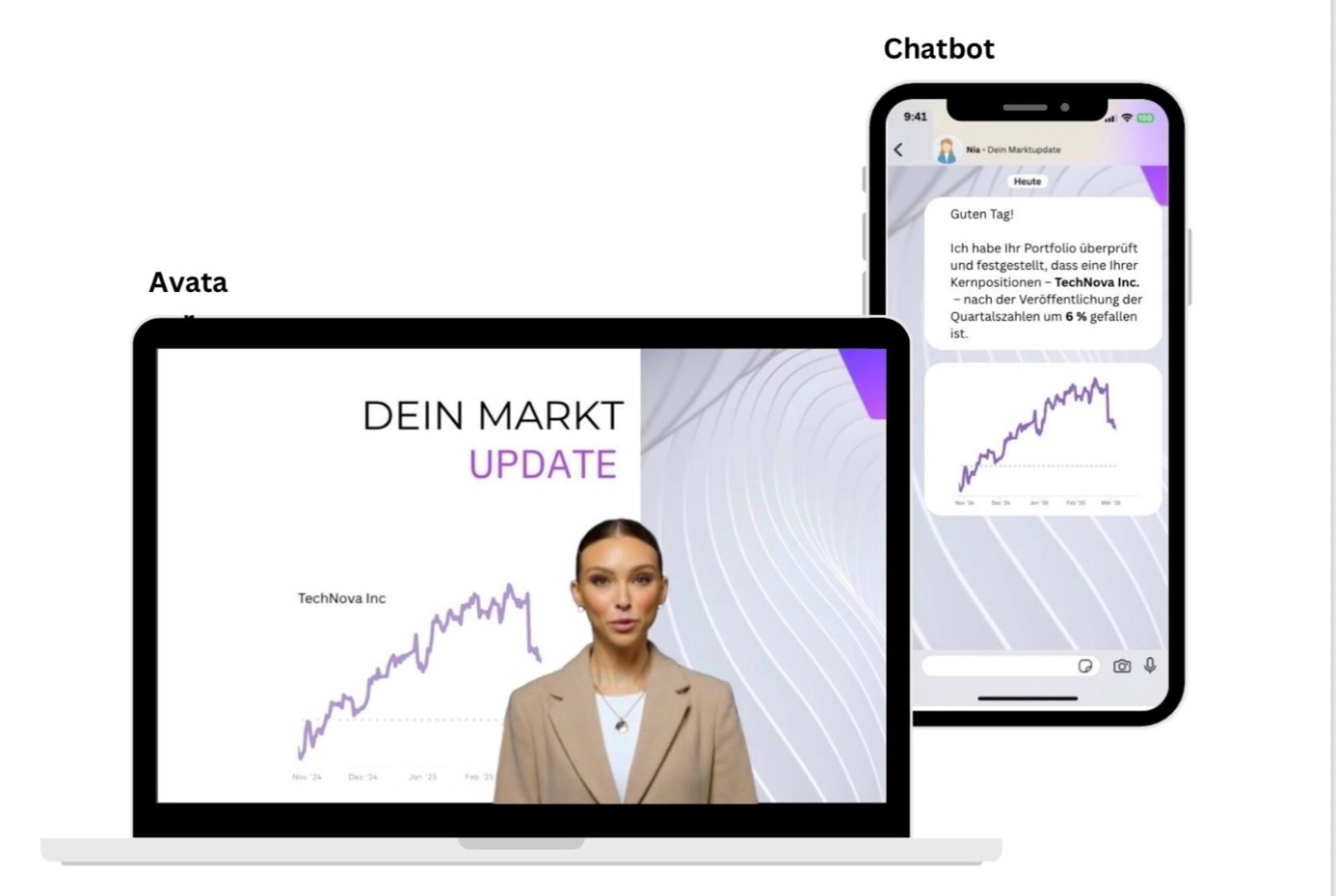

The bachelor thesis by Svetlana Pobivanz examines how AI autonomy and communicative interaction design influence trust in AI-based investment advice, which is essential for the adoption of digital banking and robo-advisory services.

Research Objective:

The study investigates the role of AI system characteristics—autonomy and interaction style—on user trust. While previous research (Lee & See, 2004; Siau & Wang, 2018) highlighted trust as central to technology acceptance, this study extends this by considering the psychological and design-related factors affecting trust in financial AI.

Specifically, the research explores whether a semi-autonomous AI with user choice or a fully autonomous AI, and whether a human-like avatar or a text-based chatbot, can enhance perceived trustworthiness.

Method:

A 2×2 experimental design was employed with 197 participants who were randomly assigned to one of the four experimental conditions. Participants interacted with a fictional AI portfolio assistant simulating investment recommendations.

In the full-autonomy condition, the AI made decisions independently.

In the semi-autonomy condition, the AI offered three options for the user to select.

The interaction design varied between a human-like avatar capable of speech and facial expressions and a text-based chatbot.

Trust was assessed using the Trust in Automation Scale (Jian et al., 2000) and the Trust in Artificial Intelligence Scale (Hoffman et al., 2021), evaluating perceived reliability, competence, and transparency.

Illustration of how the avatar and chatbot were displayed during the survey.

Key Findings:

Contrary to expectations, neither AI autonomy nor interaction design had a significant main effect on trust (p > .05). Descriptively, avatar-based advisors were perceived as slightly more personable, but this did not translate into significantly higher trust.

A regression analysis revealed that participants’ general attitudes toward AI were the strongest predictor of trust (b = .53; β = .45). Positive prior attitudes toward AI consistently led to higher trust, irrespective of system design. This aligns with the Technology Acceptance Model (Venkatesh & Davis, 2000), emphasizing trust as a key determinant of technology adoption.

Conclusion:

The results of the study show that trust in AI-supported investment advice depends less on interaction design or degree of autonomy. Neither avatars nor chatbots nor different levels of autonomy had a significant impact on trust. Although avatars are perceived as more likeable, this effect did not translate into greater trust.

Rather, the general attitude of users towards AI is decisive. It can be confirmed that trust is primarily created through transparency, traceability and comprehensible communication (Hoffman et al., 2023; Choung, David & Ross, 2023). User-friendly presentations can improve the experience, but they do not replace the need for clear explanations and education.

Overall, the results show that promoting knowledge, transparency and a positive attitude is key to building trust in AI-based investment advice and strengthening the acceptance of such systems in the long term.

References:

Choung, H., David, P., & Ross, A. (2023). Trust in AI and Its Role in the Acceptance of AI Technologies. International Journal of Human–Computer Interaction, 39(9), 1727–1739. https://doi.org/10.1080/10447318.2022.2050543

Hoffman, R. R., Mueller, S. T., Klein, G., & Litman, J. (2023). Measures for explainable AI: Explanation goodness, user satisfaction, mental models, curiosity, trust, and human-AI performance. Frontiers in Computer Science, 5, 1096257. https://doi.org/10.3389/fcomp.2023.1096257

Jian, J.-Y., Bisantz, A. M., & Drury, C. G. (2000). Foundations for an Empirically Determined Scale of Trust in Automated Systems. International Journal of Cognitive Ergonomics, 4(1), 53–71. https://doi.org/10.1207/S15327566IJCE0401_04

Lee, J. D., & See, K. A. (2004). Trust in Automation: Designing for Appropriate Reliance. Human Factors: The Journal of the Human Factors and Ergonomics Society, 46(1), 50–80. https://doi.org/10.1518/hfes.46.1.50_30392

Siau, K., & Wang, W. (2018). Building Trust in Artificial Intelligence, Machine Learning, and Robotics. 47https://www.researchgate.net/publication/324006061_Building_Trust_in_Artificial_Intelligence_Machine_Learning_and_Robotics

Venkatesh, V., & Davis, F. D. (2000). A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Management Science, 46(2), 186–204. https://doi.org/10.1287/mnsc.46.2.186.11926

The ongoing digitalization has not only transformed consumer behavior but also revolutionized how companies target their audiences. Particularly in the cosmetic industry, influencer marketing has become increasingly relevant. A novel development in this area is the rise of virtual influencers (VI), created using computer-generated imagery (CGI). In her master’s thesis, Julia Mergel, a student of our business psychology program, explores the effects of the visual human-likeness of VI on their perceived credibility in the cosmetic industry. The study identifies key factors for successful collaborations between companies and VI.

Research goal

The goal of this research was to understand how the visual human-likeness of VI affects their credibility ratings. The focus on credibility is especially relevant for virtual influencer, because – unlike human influencers – they are not independent entities and every post by them is usually created by a marketing team in the background. The study focuses on the cosmetic industry, where credibility plays a crucial role in consumer purchase decisions. Specifically, the research investigates whether different degrees of human-likeness in VI affect three critical factors influencing credibility: attractiveness, trustworthiness, and expertise. These three factors are related to each other in an interdependent relationship, collectively creating the perception of credibility of news senders (Ohanian, 1990).

Research overview

VI are CGI-created characters that actively participate in social media and are increasingly used for marketing purposes. Their application is particularly noticeable in the fashion and cosmetic industries. However, up to now the majority of studies on influencer marketing has primarily concentrated on human influencers (Why are influencers perceived as credible by social media users? – Innovation Acceptance Lab), with few focusing on virtual influencers and even fewer examining the effect of visual human-likeness on VI credibility.

The participants in the study were exposed to four different influencers: three VI with varying degrees of human-likeness and one human influencer. The study employed a within-subjects design where each participant viewed all influencers with a different post on a cosmetics product in a randomized order. The VI ranged from highly animated, cartoonish depictions to almost photorealistic, human-like virtual influencers. Participants were then asked to rate the credibility of each influencer and, in addition, to evaluate the three factors underlying credibility: attractiveness, trustworthiness, and expertise, which were later used as mediators in the analysis.

The study was run as an online experiment involving 119 female Instagram users, all of whom followed influencers.

Main findings

The study revealed that visual human-likeness significantly influences the perception of credibility. It was found that greater human-likeness had a positive impact on credibility ratings up to a certain point: No significant difference in perceived credibility was found between the most human-like VI and the human influencer.

The degree of human-likeness also had an effect on the underlying credibility factors:

Trustworthiness: A higher degree of human-likeness had a significant positive influence on trustworthiness of the VI.

Attractiveness: A higher degree of human-likeness also increased the perceived attractiveness of the VI. Attractiveness plays a central role in credibility evaluations of influencers, as this trait fosters trust among consumers, making the VI appear less „uncanny“ or artificial (Choudhry et al., 2022).

Expertise: The perceived expertise of VI also increased with greater human-likeness. Participants perceived human-like VI as more competent compared to highly animated ones.

The parallel mediation analysis confirmed that all three factors influencing credibility—attractiveness, trustworthiness, and expertise—served as mediators. Overall, 72.5% of the total variance in credibility ratings was explained after including these mediators (p < .001). Trustworthiness, in particular, had the strongest effect on credibility assessments.

Scepticism toward influencer marketing

Despite the clear trends, the overall findings showed that none of the four influencers (including the human influencer!) received particularly high credibility ratings. On a seven-point scale, the highest mean score was lower than the “neutral” middle point (M = 3.71, SD = 1.32). This aligns with a survey by a digital market research institute, which found that advertising with human influencers is not necessarily perceived as more credible than traditional advertising (nextMedia. Hamburg, 2022). Thus, there may be other reasons, why influencers are so successful at the moment.

In an additional exploratory survey, reasons for and against following VI accounts were examined. Five respondents mentioned following VI out of entertainment, content interest, or curiosity. On the other hand, there were 90 negative responses. The most common reasons were that VI were seen as unrealistic, inauthentic, incapable of real experiences, and thus perceived as untrustworthy. Additionally, some found VI impersonal, and at times, even eerie or threatening. However, these descriptive results are likely influenced by the fact that VI aren’t as popular in Germany as in some American or Asian countries (Ströer Blog, 2023).

Implications

For the cosmetic industry, particularly in advertising on platforms like Instagram, companies and developers of VI should consider the following key factors to enhance the credibility of their marketing campaigns.

Visual human-likeness: Companies should opt for VI with high visual human-likeness to increase credibility and avoid consumer discomfort.

Factors influencing credibility: Companies should prioritize VI that are perceived as trustworthy, competent, and attractive to boost source credibility. Trustworthiness has the greatest impact on credibility, so particular attention should be paid to this factor.

Product categories: Products such as nail polish or lipstick, which enhance aesthetic appeal, are better suited for VI advertising than products intended to correct human flaws.

Conclusion

While there remains scepticism surrounding VI, they are increasingly gaining importance in marketing, especially in the cosmetic industry. Our study shows that greater visual human-likeness positively influences the perception of attractiveness, trustworthiness, and expertise—key factors influencing credibility. Companies should leverage these insights to tailor their marketing strategies around VI and maximize the benefits of this innovative technology.

References

Choudhry, A., Han, J., Xu, X. & Huang, Y. (2022). „I Felt a Little Crazy Following a ‚Doll'“: Investigating Real Influence of Virtual Influencers on Their Followers. Proceedings of the ACM on Human-Computer Interaction, 6(GROUP), 1–28. https://doi.org/10.1145/3492862

Ohanian, R. (1990). Construction and Validation of a Scale to Measure Celebrity Endorsers‘ Perceived Expertise, Trustworthiness, and Attractiveness. Journal of Advertising, 19(3), 39–52. https://doi.org/10.1080/00913367.1990.10673191

Digital sales consultation through AI-driven dialogue systems is increasingly shaping interactions between companies and customers. A central trend in this context is Conversational Commerce, where AI-based systems provide personalized product recommendations and advice in online shopping. With advancing technological development, these systems are becoming ever more human-like – from text-based chatbots to voice assistants that communicate naturally, and finally to AI avatars whose appearance and behavior are sometimes barely distinguishable from real people. But how does this increasing human-likeness affect user perception and acceptance? This question was at the heart of the bachelor’s thesis by Lara-Maria Kraft, which examined the influence of different AI representations – chatbot, voice assistant, and AI avatar – on users’ willingness to use such systems within the framework of Conversational Commerce.

Research Objective

The aim of the study was to examine whether a higher degree of human-likeness – that is, moving from a text-based chatbot to a voice assistant and ultimately to an AI avatar – increases users’ willingness to use these systems. In addition, the study analyzed whether this relationship is mediated by perceived human-likeness (anthropomorphism) and moderated by potential discomfort as described by the Uncanny Valley effect. The findings aim to help companies in digital commerce design AI-based tools that foster high user acceptance and thereby contribute to long-term commercial success in Conversational Commerce.

Method

The research was conducted as an experimental online study with 176 participants. Subjects were randomly assigned to one of three interaction formats differing in their level of human-likeness:

Chatbot – text-based interaction

Voice Assistant – auditory communication

AI Avatar – audiovisual representation

All groups were shown an identical video scenario simulating an AI-based product consultation in an online store. Using the example of choosing a running shoe, participants were guided through the consultation process by a virtual assistant. Afterwards, they evaluated their perception of anthropomorphism (the attribution of human qualities), their feeling of eeriness in line with the Uncanny Valley concept, and their willingness to use the presented AI system.

Key Findings

The results revealed a generally high willingness to use AI-based consultation systems in the context of Conversational Commerce – regardless of their specific form. Contrary to expectations, the degree of human-likeness had no significant impact on usage intention; no differences were found between chatbot, voice assistant, and AI avatar conditions.

Likewise, neither the mediating role of anthropomorphism nor the moderating effect of eeriness (as explained by the Uncanny Valley effect) were empirically supported. However, a clear positive relationship emerged between perceived anthropomorphism and willingness to use: the more human-like a system was perceived to be, the greater participants’ readiness to interact with it. Thus, anthropomorphism, understood as the subjective attribution of human qualities, proved to be a central factor influencing user perception and acceptance of AI tools – independent of their visual or technical design.

Practical Implications

Based on the empirical results, several practical recommendations can be derived for the design of AI-driven systems in Conversational Commerce. The findings show that users generally display a high openness to interaction with AI systems, regardless of their external form. This overall acceptance can serve as a strategic impulse for companies to systematically integrate AI-based consultation tools into digital shopping processes.

Especially in e-commerce, where personal consultation is often lacking, such systems can enhance the customer experience by supporting users throughout the information, selection, and decision-making phases. However, companies should not primarily invest in costly or hyper-realistic avatars. Instead, the focus should be on creating a natural, empathetic, and user-oriented communication style that builds trust and conveys social closeness – factors that are far more decisive for acceptance than purely visual human-likeness.

Conclusion

This study explored the influence of increasing human-likeness in AI-based systems on user acceptance within the field of Conversational Commerce. Contrary to expectations, the degree of human-likeness – whether chatbot, voice assistant, or AI avatar – did not significantly affect users’ willingness to engage. What truly matters is how human-like the system is perceived.

Perceived anthropomorphism emerged as a key factor: the more human qualities users attributed to a system, the greater their willingness to use it – independent of its actual design. However, this perception is not necessarily triggered by more human-like visual appearance alone.

Future research should therefore focus on identifying the specific factors and interaction elements that foster anthropomorphism in AI systems – and explore how these can be strategically employed to further enhance user acceptance and experience.

This study explores how anthropomorphic factors influence the acceptance of AI-generated singing. By building upon classical acceptance models like TAM and UTAUT2, we incorporate concepts such as animacy, humanlike fit, and perceived sociability. Utilizing a quantitative survey with 310 participants and analyzing the data through PLS-SEM, the study finds that animacy and humanlike fit are significant predictors of likeability, which then positively influences the intention to use AI-generated singing. Word of mouth (WoM) and curiosity also emerge as critical drivers of acceptance.

The study suggests that listeners primarily respond to the expressive qualities of AI singing (animacy and humanlike fit), while perceived sociability remains largely irrelevant. This highlights a limitation of classical acceptance models, which do not account for the anthropomorphic appeal of AI-generated creative content. Future research should address these factors, especially as AI continues to advance in creative domains.

Full citation:

Bagratuni, M., Müller, P., & Planing, P. (2025). Innovation in tune: An empirical investigation of user acceptance of artificial intelligence-generated music. Computers in Human Behavior Reports, 18, Article 100660. https://doi.org/10.1016/j.chbr.2025.100660

Our latest research on the impact of Immersion on technology acceptance is published in the renowed journal Transportation Research Interdisciplinary Perspectives and can be accessed free of charge here.

Key Findings

1. VR Dominates Immersion Quality

Among the three media conditions, VR emerged as the most immersive format. Participants using VR reported a significantly higher sense of presence and engagement compared to those exposed to videos or photos. This heightened immersion translated into richer emotional and cognitive responses, showcasing VR’s potential to create powerful, near-real experiences of using air taxis.

2. Immersion Does Not Equate to Immediate Adoption

Surprisingly, despite VR’s superior immersion quality, the study found no significant differences in participants‘ intention to use air taxis across the three media formats. While VR enhanced emotional engagement, it did not directly translate into higher immediate adoption intentions. This highlights the complexity of the decision-making process and suggests that factors beyond immersion—such as cost, safety, and accessibility—may play a more prominent role in shaping long-term acceptance.

3. Multifaceted Decision-Making in VR

VR’s impact extended beyond basic adoption intentions. Participants in the VR condition considered a broader array of factors, including reliability and social influence, when evaluating air taxis. This suggests that VR experiences prompt users to engage in more comprehensive and nuanced decision-making processes, balancing both emotional and utilitarian considerations. For instance, VR users were more likely to assess air taxis‘ reliability, reflecting their ability to visualize safety features and operational scenarios in greater detail.

Implications for Industry and Policymakers

Enhancing Engagement Through Immersion

For companies and policymakers promoting air taxis, the findings underscore the importance of immersive technologies. VR can bridge the gap between abstract concepts and tangible experiences, allowing users to virtually „test“ air taxis before they become a reality. This approach can help address common concerns, such as safety and reliability, while building emotional connections with the technology.

Strategic Media Choices

While VR offers unparalleled immersion, the study also highlights the cost-effectiveness of using less immersive media like photos or videos in certain contexts. For example, initial awareness campaigns may benefit from these formats, which are easier and cheaper to produce, while VR can be reserved for targeted initiatives aimed at deepening user engagement and addressing specific adoption barriers.

Addressing Broader Acceptance Factors

The lack of significant differences in adoption intention across media formats suggests that technological acceptance hinges on more than just immersive experiences. Policymakers and developers must address critical factors such as affordability, accessibility, and environmental impact to foster widespread adoption. Immersive technologies should complement these efforts, providing users with a holistic understanding of air taxis’ benefits and addressing potential concerns.

The Power of VR in Shaping Perceptions

One of VR’s unique strengths lies in its ability to evoke emotional responses. By simulating realistic scenarios, VR can make futuristic technologies feel tangible and relatable. For air taxis, this means giving users a sense of what it’s like to soar above cityscapes, experience smooth takeoffs and landings, and visualize safety protocols in action. These experiences not only build excitement but also help demystify the technology, reducing apprehension and fostering trust.

Limitations and Future Directions

While the study provides valuable insights, it also acknowledges certain limitations. The sample consisted primarily of university students, limiting the generalizability of the findings. Future research should involve more diverse demographics to capture a broader range of perspectives. Additionally, the study focused on three specific media formats; exploring other immersive technologies, such as augmented reality or interactive demonstrations, could provide a more comprehensive understanding of how media influences technology acceptance.

Conclusion

The adoption of innovative technologies like air taxis depends on a delicate balance of emotional and rational factors. While immersive media formats like VR hold immense potential to enhance engagement and address user concerns, they are not a standalone solution. Industry stakeholders must take a multifaceted approach, combining immersive experiences with practical considerations like cost and accessibility. By leveraging the unique strengths of VR and addressing broader acceptance factors, we can pave the way for a future where air taxis become a seamless part of urban mobility.

Our cities face significant challenges, particularly regarding mobility and quality of life. Increasing traffic and the associated environmental impacts are progressively affecting urban life. The need to make mobility more sustainable is now ever-present, which goes along with an acceptance of the suggested changes. „Every change means that a person has to leave his known and habitual actions, his environment, his habits, his role, in short his status quo“(Frey et al., 2008, p. 281). A key question, therefore, is: How can the acceptance of sustainable mobility be increased among citizens? This is precisely where Joshua Klein’s bachelor thesis comes in, conducted as part of the research project „Streetmoves4iCity“ (read more here about this project). The thesis explores how immersive technologies like Virtual Reality (VR) and Augmented Reality (AR) can help to increase citizens’ acceptance of traffic-reducing measures by making the positive effects of the change visible.

Virtual Reality (VR): Creates a fully digital environment in which the user immerses themselves. Using headsets, the real world is completely blocked out, and the user is placed in a computer-generated world that is interactive and immersive.

Augmented Reality (AR): Overlays digital information onto the real world. Using smartphones or glasses, users see the real environment, enhanced with digital elements.

Research goal: The aim of the study was to determine whether and to what extent immersive technologies can promote the acceptance of measures aimed at reducing urban road traffic by visualizing the positive effects of these measures. Specifically, it examined whether VR and AR are perceived differently and how immersion—the feeling of being absorbed in a virtual environment—impacts acceptance. These questions are crucial, as the successful implementation of sustainable mobility concepts often depends on the public’s willingness to accept change.

Research overview: The empirical study was conducted in the Leonhardsvorstadt district of Stuttgart and aimed to simulate the experience of traffic-reducing measures through VR and AR. The investigation involved two independent groups: one group experienced the planned measures through a VR simulation, while the other group used AR. The VR group was shown a 360-degree video of a previously implemented traffic trial in Mannheim (see here for another study using this methodology), while the AR group experienced a live augmented reality simulation using a Microsoft HoloLens2 mixed-reality head-mounted display. In both cases, participants’ acceptance of the measures was assessed both before and after the experience, along with their perceived immersion. A total of 44 people took part in the study.

The central hypothesis was that the experience of the positive effects of traffic-reducing measures through VR and AR would lead to a significant increase in acceptance of these measures. Additionally, the study examined whether there were differences in perceived immersion between the two technologies and whether this mediated the effect on acceptance. Another research goal was to explore whether familiarity with the respective technology influenced immersion.

The study was supplemented by qualitative interviews to identify what is currently lacking in public spaces in the Leonhardsvorstadt, how car parking spaces can be used more efficiently, and what suggestions participants had for improving public spaces by reducing traffic flow.

Main results

Increased acceptance: First, it was confirmed that both VR and AR can contribute to increasing the acceptance of measures aimed at reducing urban road traffic. This is an important finding, as it shows that immersive technologies can be valuable tools for citizen participation and urban planning.

VR and AR are equally convincing: Interestingly, there were no significant differences between the two technologies in terms of their effect on acceptance. Both VR and AR were equally convincing to participants. This suggests that both technologies are equally suitable for involving citizens early in planning processes and demonstrating the benefits of traffic measures.

Level of immersion has no effect: Surprisingly, the perceived immersion played a smaller role than expected. The results suggest that it is less about the depth of the immersive experience and more about making changes tangible and understandable. Even a high level of immersion does not necessarily lead to a change in opinion, as the impact depends more on the conveyed facts.

No mediation by familiarity with technology: Another question was whether familiarity with the respective technology could influence the perceived immersion. However, this assumption was not confirmed. Participants’ familiarity with VR or AR had no significant effect on their immersion experience. Therefore, even people with little experience with these technologies could benefit from their use.

Desire for parks, leisure facilities, and cleanliness: The qualitative responses emphasized an improvement in quality of life. Park-like structures were often desired, followed by an expansion of sustainable infrastructure, gastronomy, cultural offerings, and improved cleanliness in the district.

Conclusion

In summary, Joshua Klein’s thesis demonstrates that both virtual and augmented reality are effective tools for promoting the acceptance of measures aimed at reducing urban road traffic. The immersive experience of such measures through technologies like VR and AR gives citizens the opportunity to realistically perceive planned changes and better understand their benefits. A key advantage of the technology is that it not only stimulates citizens‘ imagination but also helps reduce uncertainties and build trust in the feasibility of such measures. These findings offer valuable insights for urban planning and citizen participation, particularly concerning the planning of sustainable mobility concepts. With VR and AR, cities like Stuttgart have an effective means of involving citizens early in planning processes and illustrating the positive impact of such projects on quality of life.

Frey, D., Gerkhardt, M. & Fischer, P. (2008). Erfolgsfaktoren und Stolpersteine bei Veränderungen. In D. Beck, R. Fisch, A. Müller & D. Beck (Hrsg.), Veränderungen in Organisationen: Stand und Perspektiven (S. 281- 299). VS Verlag für Sozialwissenschaften. https://doi.org/10.1007/978- 3-531-91166-3

In an era in which advertising spending has risen excessively despite the flood of information, only about 5% of messages struggle to get the attention of potential consumers (Kroeber-Riel, 2015). Especially in saturated markets, such as the Fast Moving Consumer Goods (FMCG) sector, advertisers are subjected to a high level of competitive pressure (Naderer et al., 2011). Today’s demand for advertising spots is clear: they need to stand out and catch attention in order to be effective at all (Levenson, 2011).

In this challenging environment, emotional marketing relies on the influence of the decision-making process without presenting offering rational arguments. Our latest study aimed at highlighting the effectiveness of more emotional compared to informative advertising. The central question was to find most effective advertising strategies to have a sustainable impact on respective target groups.

Research objective:

The study was conducted by Svenja Greitmann and takes a look at the world of advertising in the midst of a real abundance of information. The aim was to assess the effectiveness of emotional compared to informative advertising in the field of Fast Moving Consumer Goods (FMCG). It further investigated differences with regard to gender and product categories. The outcome may be helpful for companies looking for the most effective advertising strategies.

Method:

Based on a preliminary study, two product categories were selected, one that was utilitarian (glass cleaner) and one that was hedonic (soft drink).

For each category a product from a fictitious brand was created. And for each product, two social media spots were made that either were emotional (e.g., by showing positive pictures like smiling people using the product) or information (e.g., by giving positive information about product ingredients). The emotional spot was expected to be especially effective with the hedonic product, whereas the informational spot should be more effective with the utilitarian product.

The main study had an experimental 2x2x2 factor-between-subject design to examine cause-effect relationships. Participants were randomly assigned to one of four advertising spots to systematically measure the impact of advertising appeals and product categories. In addition, gender of participants was assessed.

Sample:

The sample consisted of 185 adults.

Key Findings:

Contrary to our expectations, the study showed overall an advantage of the informational over the emotional spots. However, there was also a three-way interaction found. For men, the expected interaction pattern showed, i.e. emotional spot was more effective with the hedonic product, whereas the informational spot was more effective with the utilitarian product.

This effect was not found for women, which may be due to a different relevance of nutrition and health information when buying a soft drink. This may explain, why informational advertising was more effective with soft drinks for female participants.

Thus, informational advertising seems to be relevant if the product category shows a higher level of involvement (e.g., due to health issues)

Conclusion:

This study investigated the effectiveness of emotional and informative advertising on two different Fast Moving Consumer Goods. The results showed that informative advertising is superior, contrary to the assumption that emotional stimuli should be more effective with low-involvement products. There is a need to clearly understand the relevance of a product for a selected target group in order to find the best advertising strategy. Overall, advertising research remains relevant in the face of changing consumer needs, but requires continuous adaptation and refinement of advertising strategies.

References

Kroeber-Riel, W. (2015). Strategie und Technik der Werbung: Verhaltenswissenschaftliche und neurowissenschaftliche Erkenntnisse. Stuttgart: Kohlhammer.

Naderer, G., Balzer, E. & Batinic, B. (Hrsg.). (2011). Qualitative Marktforschung in Theorie und Praxis: Grundlagen, Methoden und Anwendungen. Wiesbaden: Gabler.

The prevalence of adult obesity has more than doubled worldwide since 1990 (World Health Organization [WHO] 2024). Obesity-related diseases caused about 11% of deaths in 2019 (WIOD, 2022). A healthy diet is recommended to prevent obesity; however, only few consumers are interested in learning about this topic (IfD Allensbach, 2023, as cited in Statista, 2023).

Front-of-pack (FOP) labels, particularly the Nutri-Score, can be used to address this problem. Nutritional values, which are otherwise only shown in a nutritional value table, usually on the back of a package, are summarized using the Nutri-Score. This allows consumers to quickly judge how nutritious selected products are in comparison.

The EU plans to introduce a binding FOP label (European Parliament, 2022, 2023). Studies have shown that the conceptual understanding of the Nutri-Score must be improved to ensure its’ effective use (Liu et al., 2014). However, it remains unclear whether consumers know how to use the Nutri-Score accurately. This post summarizes research examining consumers’ conceptual understanding of the Nutri-Score.

Research aim:

In the present study conducted by Nicole Del, the conceptual understanding of the Nutri-Score was examined and compared with other forms of understanding, namely subjective and objective understanding. It was further investigated whether gender and the involvement in healthy nutrition have an influence on conceptual understanding.

Method:

This study examined the extent to which consumers correctly understand the Nutri-Score. In the survey, different aspects of understanding were assessed using a sample of 170 consumers (aged 18-78 years).

Objective understanding was assessed by letting participants choose the healthiest and unhealthiest options from three products within a product category. Each product had a different Nutri-Score. They had to make a choice for five different product categories. The number of correct choices was translated into an objective score.

Subjective understanding was measured through self-assessment using a rating scale from 1 (I do not understand at all) to 10 (I understand very well).

Conceptual understanding was measured using ten true-false statements. The score was based on correctly categorizing the statements as true or false.

Key results:

Consumers’ conceptual understanding of the Nutri-Score was lower than that of the other forms (conceptual 63%, objective 85%, subjective 70%).

Thus, consumers do not have a sufficient conceptual understanding of the Nutri-Score for the correct application. Over half of the participants mistakenly thought that foods with a Nutri-Score of D or E should not be consumed, and over 40% believed that a Nutri-Score of A or B indicates that the food is healthy (both are not correct).

Interestingly, subjective, objective, and conceptual understanding did not correlate, implying that they constitute different dimensions of understanding.

Neither gender nor involvement in healthy eating had a significant influence on conceptual understanding.

Summary:

The EU’s Farm-to-Fork Strategy plans to introduce a binding FOP label. Currently, the Nutri-Score is one of the most widely used FOP labels in the EU. If properly applied, the label can reduce the number of consumers with diet-related diseases by guiding healthy food choices (Egnell et al., 2019). However, our study shows that many consumers do not understand the label sufficiently. They have knowledge gaps in their conceptual understanding of the label, implying that they may not always correctly apply the Nutri-Score. Thus, there is a need for informational campaigns to explain the meaning of the Nutri-Score.